XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher high area of the channel

XAUUSD – Gold price maintains near record highs of $2,300 amidst weak US Dollar

The Gold prices are moving higher ahead of US Non- Farm Payrolls scheduled today, and expected 200k versus 275K printed in the previous reading. US FED Members believed that inflation will not come down in the near term, So rates will be sustained for longer time as higher rates. So Gold prices are come to little pressure of holding Gold in the locker rate will be higher for long time.

Gold price remains near record highs of $2,300 as the weak US Dollar continues to provide support. The decline in the US Dollar was prompted by the disappointing United States Institute for Supply Management (ISM) Services PMI report for March.

Additionally, 10-year US Treasury yields drop to 4.34% amid positive market sentiment. Market expectations for the Federal Reserve (Fed) to initiate a reduction in its interest rate stance at the June meeting have also eased. According to the CME FedWatch tool, traders now price in a 58% chance of a rate cut in June, down from 70% a week ago.

Investors are eagerly awaiting the release of the US Nonfarm Payrolls (NFP) report for March, scheduled for Friday. Projections suggest that US employers added 200K new payrolls during the month, a decrease from the previous reading of 275K. The Unemployment Rate is anticipated to remain stable at 3.9%. Average Hourly Earnings, a key indicator of wage growth and inflation, are expected to rise at a slower pace of 4.1% year-on-year compared to 4.3% in February.

Strong wage growth and labor market demand could temper expectations for a Fed rate cut in June, while weaker labor market conditions may increase hopes for rate cuts. The latter scenario could potentially drive down US yields and bolster Gold prices further.

In the late European session, the US Department of Labor reported higher-than-expected weekly jobless claims data for the week ending March 29. Initial jobless claims rose to 221K, exceeding expectations of 214K and the previous reading of 212K, which was revised upward from 210K.

EURUSD – ECB Accounts: Rate Cut Consideration Gaining Strength

The Accounts of ECB bank monetary policy meeting outcome is rate cuts in upcoming months is more possible and ECB Members agreed with inflation is trending down towards to 2% target. Wage Growth is moderating and domestic data showing downturn in all Euro areas. We need confidence in more upcoming data to cut the rates in upcoming months.

EURUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

EURUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

The accounts of the European Central Bank’s (ECB) March policy meeting, released on Thursday, highlighted several key points regarding the economic outlook and inflation in the Eurozone:

- Progress was observed across all fronts, suggesting increased confidence in the ECB’s target of achieving inflation rates consistent with its goals.

- However, the Governing Council emphasized the need for additional data and evidence to bolster this confidence further.

- Expectations pointed towards a potentially uneven trajectory for inflation, with a projected dip following the summer period.

- Signs indicated a potential moderation in wage growth, contributing to the overall assessment of inflation dynamics.

- Members of the Governing Council expressed growing confidence in the prospects of inflation gradually declining towards the ECB’s 2% target.

- Despite the positive developments, caution was advised, emphasizing the fragile nature of the disinflationary process.

- Notably, the accounts suggested that the rationale for contemplating rate cuts was becoming more compelling, indicating a shift towards potential monetary policy adjustments in response to the evolving economic conditions.

USDCAD – climbs past 1.3560, eyes on US and Canadian job figures

The Canadian Trade surplus for the month of February came at $1.39Billion from $0.61 Billion in Previous month. This is the positive news for Canadian economy and Oil prices continued to support for Canadian Dollar amid rising tensions of Geopolitical nations.

USDCAD is moving in the Box pattern and the market has rebounded from the support area of the pattern

During the early European trading session on Friday, the USD/CAD pair is seen gaining momentum, approaching the 1.3565 mark. This surge is attributed to renewed demand for the US Dollar (USD) amid escalating geopolitical tensions in the Middle East, which are driving investors towards safe-haven assets.

Federal Reserve (Fed) Bank of Richmond President Thomas Barkin’s remarks on Thursday contributed to the strengthening of the USD. Barkin expressed expectations of continued disinflation, albeit uncertain about its pace. He emphasized the importance of maintaining somewhat restrictive interest rates to steer inflation back towards the target level. Fed Chair Jerome Powell echoed similar sentiments, indicating that if the economy progresses as anticipated, it might be appropriate to commence lowering policy rates.

Market participants eagerly await the release of the US labor market data for March, scheduled for Friday, as it will provide crucial insights into the Fed’s stance on interest rates. The highly-anticipated Nonfarm Payrolls (NFP) report is expected to reveal a job addition of 200,000 in March, following a notable increase of 275,000 in February. The Unemployment Rate is anticipated to remain unchanged at 3.9% for the same period. A stronger-than-expected NFP reading could reduce expectations of a rate cut by the Fed in June, lending support to the USD and propelling the USD/CAD pair higher.

On the Canadian front, positive economic indicators such as an increased trade surplus of $1.39 billion in February, up from $0.61 billion in January, have bolstered the Canadian Dollar (CAD). Moreover, the surge in oil prices, driven by heightened tensions in the Middle East, has provided additional support for the commodity-linked Loonie. These factors may act as a limiting factor for the upside potential of the USD/CAD pair. Traders will closely monitor the release of Canadian labor market data later in the day for further market direction.

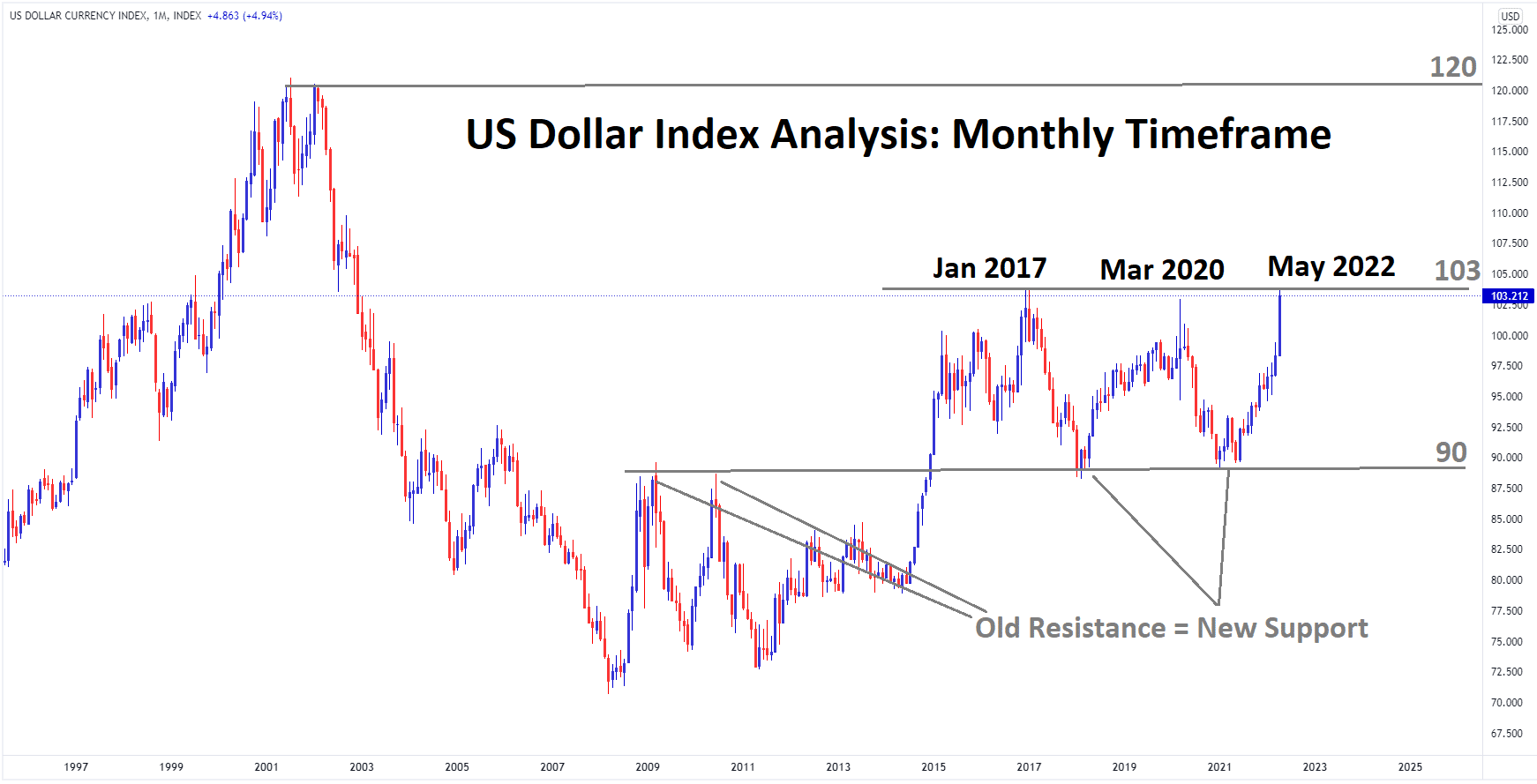

USD INDEX – Goolsbee: Housing Price Pressures Pose Biggest Inflation Threat

The Chicago FED President Austan Goolsbee said US Housing market is robust higher, this higher prices of rates is difficult to come down the inflation to our target of 2%. Housing prices will come down if rates sustained longer time for higher, then Employment rate also cooled down. Rate cuts is not seen when inflation did not come to our target of 2%.

USD INDEX is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

Chicago Federal Reserve Bank President Austan Goolsbee emphasized on Thursday that the persistently high price increases in the housing services sector pose the most significant obstacle to the Federal Reserve’s efforts to bring inflation down to its target rate of 2%.

Goolsbee further elaborated on this issue:

– “If housing inflation does not come down, it would be very difficult to return inflation to 2%.”

– “I had been expecting it to come down more quickly than it has.”

– “Housing inflation is my most valuable indicator for the immediate future.”

– “Inflation in core services excluding housing has come down more than expected.”

– “The last two months of inflation data show a bump; we can’t write it off as purely noise.”

– “Risks to inflation and employment mandates have moved into better balance.”

– “If we stay restrictive for too long, we will likely see employment begin to deteriorate.”

USDCHF – rebounds near 0.9030 ahead of US labor data

The Iran retailiation attack on Israel is much waiting from Global markets, This week earlier Israel killed 2 Iranian Military generals and 5 Military peoples in Syria Iranian Emabassy.

USDCHF is moving in an Ascending channel and the market has fallen from the higher high area of the channel

Israel attacked Gaza terrorists but Missiles attacked Iran embassy on missed targets of Syrian Terrorists. Swiss CPI came at 0.0% in March month versus 0.30% increase expected and 0.60% printed in previous month. The Swiss Franc is moved lowered after the domestic data printed lower than expected.

On Thursday, amidst escalating geopolitical tensions in the Middle East, the Swiss Franc (CHF) exhibited strength, bolstered by increased market caution. The tension arose following Iran’s vow to retaliate against Israel’s attack on Iran’s embassy in Syria, resulting in casualties among Iranian military personnel.

In economic news, the Swiss Consumer Price Index (CPI) for March delivered a lackluster performance, showing no change on a month-over-month basis, falling short of expectations which had anticipated a 0.3% increase. Additionally, the year-over-year CPI figure rose by 1.0%, lower than both the anticipated 1.3% and the previous month’s reading of 1.2%. This softer-than-expected CPI data has raised speculations of another interest rate cut by the Swiss National Bank (SNB).

Meanwhile, the US Dollar (USD) faced downward pressure on Thursday, primarily driven by weaker employment data from the United States (US). However, the downward trajectory of the USD was partially offset by neutral comments from several Federal Reserve officials.

Thomas Barkin, President of the Federal Reserve Bank of Richmond, highlighted the expectation of persisting disinflation, though uncertainty persists regarding the pace of this trend. Loretta Mester, President of the Federal Reserve Bank of Cleveland, expressed readiness to decrease the pace of securities runoff from the Fed’s balance sheet in the near future. Additionally, she hinted at the possibility of lowering the fed funds rate later in the year.

USDJPY – BoJ’s Ueda: Previous import cost hikes’ effect on Japan’s inflation to fade

The BoJ Governor Ueda said past prices increased in import costs will down the inflation soon. We are going to end the Government Energy subsidy and will support inflation prices higher. The Firms agreed on wage hikes also support inflation to move higher.

USDJPY is moving in the Box pattern and the market has rebounded from the support area of the pattern

Bank of Japan (BoJ) Governor Kazuo Ueda stated on Friday that he anticipates the “impact of past rises in import costs on Japan’s inflation likely to dissipate.” This suggests that the previous increases in import costs that contributed to inflation are expected to diminish in their effect over time.

Ueda also mentioned that the scheduled end to government energy subsidies is likely to affect inflation in the future. This implies that the conclusion of government subsidies for energy could have an impact on the trajectory of inflation moving forward.

Furthermore, Ueda commented on the outcome of annual wage talks, indicating that based on the results thus far, trend inflation is expected to gradually accelerate. This suggests that the trends observed in annual wage negotiations could contribute to a gradual increase in inflation over time.

GBPUSD – GBP rises further on UK’s better economic outlook, weak USD

The bank of England decision Maker Panel survey conducted for February month shows wages and Businessess selling prices will be cooled down in the next year . According to the survey , Selling prices is declined to 4.1% from 4.3%, it is the lower reading in the last 2 years. Wage growth is declined to 4.9% in the 3 month average basis from 5.2% in February month.

GBPUSD is moving in the Box pattern and the market has rebounded from the support area of the pattern

The GBP/USD pair is demonstrating strength as recent economic indicators from the United Kingdom indicate a trajectory toward economic recovery after experiencing a technical recession in the latter half of 2023. Additionally, the softening of the US Dollar, attributed to disappointing data from the United States Institute of Supply Management (ISM) Services PMI for March, has further bolstered the Cable.

In March, the UK’s Manufacturing PMI unexpectedly expanded following 20 consecutive months of contraction, primarily driven by robust domestic demand. This strong performance in the UK’s manufacturing sector has elevated business optimism to its highest level since April 2023, with 58% of manufacturers anticipating an increase in production levels over the next 12 months. Furthermore, British house prices experienced a 1.6% rise in March, marking the fastest pace since December 2022, indicating resilience in the real estate sector despite historically high interest rates.

During the European session, the latest Bank of England (BoE) Decision Maker Panel (DMP) survey for February revealed that most firms anticipate a cooling down of selling prices and wage inflation over the next year. Selling price expectations decelerated to 4.1% from 4.3%, marking the lowest reading in over two years, while wage growth expectations softened to 4.9% on a three-month moving average basis from 5.2% in February.

Market activity reflects the Pound Sterling advancing to 1.2660 against the US Dollar, with bullish sentiment prevailing and the weak US ISM Services PMI exerting downward pressure on the US Dollar. The S&P 500 commences Thursday’s session on a positive note.

The US Dollar weakened notably following the unexpected decline in the US Services PMI to 51.4 in March from expectations of 52.7 and the previous reading of 52.6. Given that the service sector constitutes two-thirds of the US economy, the adverse impact on the US Dollar was significant, with the US Dollar Index (DXY) dropping by over 0.5% to 104.15. Moreover, the ISM report indicated substantial declines in the new orders and prices paid sub-indexes.

Market focus shifts to the US Nonfarm Payrolls (NFP) report for March, set to be released on Friday, which will substantially influence market expectations regarding potential interest rate reductions by the Federal Reserve from the June meeting. The NFP report is anticipated to reveal the addition of 200K workers during the month, down from February’s figure of 275K.

In the UK, market sentiment regarding potential rate cuts by the Bank of England will guide the Pound Sterling. Investors anticipate the BoE to initiate a rate-cut cycle in June amid consistent slowdowns in UK inflation. BoE Governor Andrew Bailey has suggested that expectations of two or three rate cuts throughout the year are “reasonable.”

Furthermore, the S&P Global/CIPS Services PMI for March failed to meet expectations, declining to 53.1 from the anticipated and prior reading of 53.4. Tim Moore, Economics Director at S&P Global Market Intelligence, noted that while the recovery in service sector output slightly lost momentum in March, the overall outlook remains reasonably positive.

AUDUSD – AUD stabilizes with stronger USD before US Nonfarm Payrolls

The Australian Trade balance for the March month came at 7280 million versus 10400million expected and down from 10058 million printed in previous month. Exports declined by 2.2% MoM and imports increased by 4.8% versus 1.3% previous month. Building permits declined by 1.9% in February month versus 3.3% increase expected and 2.5% decline in previous month. Retail sales for the February month came at 0.30% inline with expected data.The Australian Dollar moved down after the declining data printed today.

AUDUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

Amid a mixed bag of economic indicators, the Australian Dollar (AUD) halted its upward trajectory after Australia’s Final Retail Sales remained unchanged and Trade Balance data disappointed, showing a narrower surplus than anticipated in March. The US Dollar (USD), on the other hand, faced pressure due to soft labor market data released the previous day, supporting the AUD/USD pair.

Australia’s Trade Surplus for March fell short of expectations, narrowing to 7,280 million compared to the anticipated 10,400 million. Exports declined by 2.2%, contrasting with the previous month’s increase of 1.6%, while Imports grew by 4.8%.

The US Dollar Index (DXY) remained subdued, reflecting a decrease in US Treasury yields and neutral remarks from several Federal Reserve officials. However, geopolitical tensions escalated following Israel’s attack on Iran’s embassy in Syria, prompting cautious market sentiment. Investors awaited US labor market data, including Average Hourly Earnings and Nonfarm Payrolls, scheduled for release on Friday.

In Australia, mixed economic data included unchanged Final Retail Sales, an improvement in the Judo Bank Services PMI, and a decline in Building Permits for February. The Reserve Bank of Australia (RBA) March minutes revealed a unanimous decision to maintain interest rates amid economic uncertainty, with the board expressing cautious optimism about balanced risks.

Federal Reserve officials expressed varied views on monetary policy, with some open to rate cuts later in the year contingent on sustained progress in inflation. US economic data for the week included a rise in Initial Jobless Claims, an increase in Challenger Job Cuts, and a higher-than-expected rise in ADP Employment Change. However, the ISM Services PMI for March weakened, indicating challenges in the service sector.

NZDUSD – nears 0.6000 before US NFP release

The Building permits for the month of February came at 14.9% MoM versus 8.6% decline in the previous month.The RBNZ is expected to keep the rates at stable in the next week meeting. The US Jobless claim benefits increased to 221K versus 212K in the march 30 reports.

NZDUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

As the markets brace for the release of crucial US labor market data, including Nonfarm Payrolls (NFP), Unemployment Rate, and Average Hourly Earnings for March, a cautious sentiment prevails.

The latest report from the Labor Department revealed that weekly Initial Jobless Claims surged to the highest level since January, reaching 221K for the week ended March 30, compared to the prior week’s 212K. Meanwhile, Continuing Claims dropped to 1.791M for the week ended March 23.

Investors are eagerly awaiting the NFP data scheduled for Friday. Forecasts suggest that the US economy added 200K jobs in March, following a 275K increase in February, with the Unemployment Rate expected to hold steady at 3.9%. A stronger-than-expected NFP figure could dampen expectations of a June Fed rate cut, providing support for the Greenback and potentially pressuring the NZD/USD pair lower. The CME FedWatch Tool indicates that markets are now pricing in nearly 65% odds of a Fed interest rate cut in June, up from 60% in the previous week.

On the New Zealand front, February’s Building Permits improved by 14.9% month-over-month, rebounding from an 8.6% decline previously, according to Statistics New Zealand. The Reserve Bank of New Zealand (RBNZ) is anticipated to maintain interest rates at its upcoming policy meeting, emphasizing the need to keep policy restrictive to anchor inflation expectations. However, any dovish adjustments to the outlook in the policy statement could weigh on the New Zealand Dollar (NZD) and pose challenges for the NZD/USD pair.

CRUDE OIL – WTI nears $86.20 amid reports of threats to Israeli embassy

The Oil prices are surged on Thursday because of Iran retaliation attacks is expected on Israel, following Iranian Military officials killed in Iranian embassy in Syria. Russia already 15% capacity down due to drone attacks from Ukraine.OPEC+ Meeting outcome is 2.2 million BPD per day output cut is declared until June month.

XTIUSD Crude Oil price is moving in an Ascending channel and the market has fallen from the higher high area of the channel.

The surge in WTI prices is fueled by escalating geopolitical tensions, particularly following an attack on Iran’s embassy compound in Syria, although Israel has not officially claimed responsibility for the incident.

Reports indicating increased threats against Israeli embassies in the United States by Iran have further heightened market concerns. Iran has vowed retaliation for an attack resulting in the death of Iranian military officials.

In addition, NATO officials revealed on Thursday that ongoing Ukrainian drone attacks on Russian refineries may have disrupted more than 15% of Russian capacity. Furthermore, a Lukoil refinery in Russia faces challenges in repairing its gasoline unit, as American firm Universal Oil Products (UOP) declined to assist Lukoil, having withdrawn from Russia after the country’s invasion of Ukraine in February 2022.

The United States imposed fresh counterterrorism sanctions related to Iran against Oceanlink Maritime DMCC, based in the United Arab Emirates, along with its vessels on Thursday. This action was taken due to the company’s involvement in shipping commodities for the Iranian military. The Treasury Department stated that these financial sanctions aim to isolate Iran and impede its ability to finance proxy groups while also supporting Russia’s conflict in Ukraine.

Amidst these developments, OPEC and its allies, known collectively as OPEC+, have decided to maintain their current oil supply policy unchanged. The voluntary production cuts, totaling 2.2 million barrels per day (bpd), will remain in effect until at least the end of June. These cuts complement the existing agreement reached in 2022, which already includes reductions of 3.66 million bpd.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – click here to see, 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!